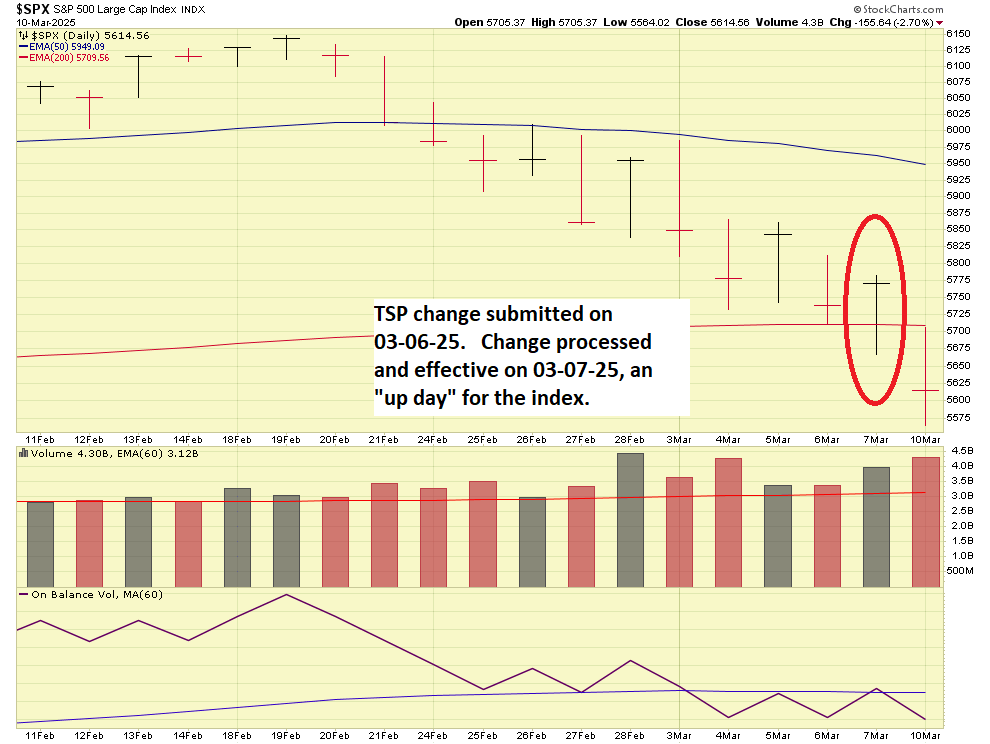

Bottom Line Up Front: I remain 100% G-Fund (a change made on March 6, almost a month ago).

Happy Liberation Day, or what is left of it. “Liberation Day”, April 2, 2025 to be exact, is when President Donald Trump announced a major trade policy shift involving the implementation of sweeping “reciprocal tariffs” on U.S. imports. This policy, unveiled in a speech from the White House Rose Garden, established a 10% baseline tariff on all imported goods, with significantly higher rates applied to specific trading partners—such as 34% on China, 20% on the European Union, and up to 46% on Vietnam—effective immediately on April 3, 2025. Trump framed this as a “declaration of economic independence,” aimed at addressing perceived trade imbalances and protecting American industries, though it marked a dramatic escalation of his administration’s trade war strategy.

A brief 15 minute analysis of this tariff policy (personally, I “see where he is coming from”, but…) is that the Trump Tariffs are basically the inverse of what NAFTA was. NAFTA, a trade agreement between Canada, US, and Mexico was actually signed by then President Bush in 1992.

Flash forward and some new thinking exists in the trade circles. Tariffs are the new policy, however while well-intended, the markets are not liking them.

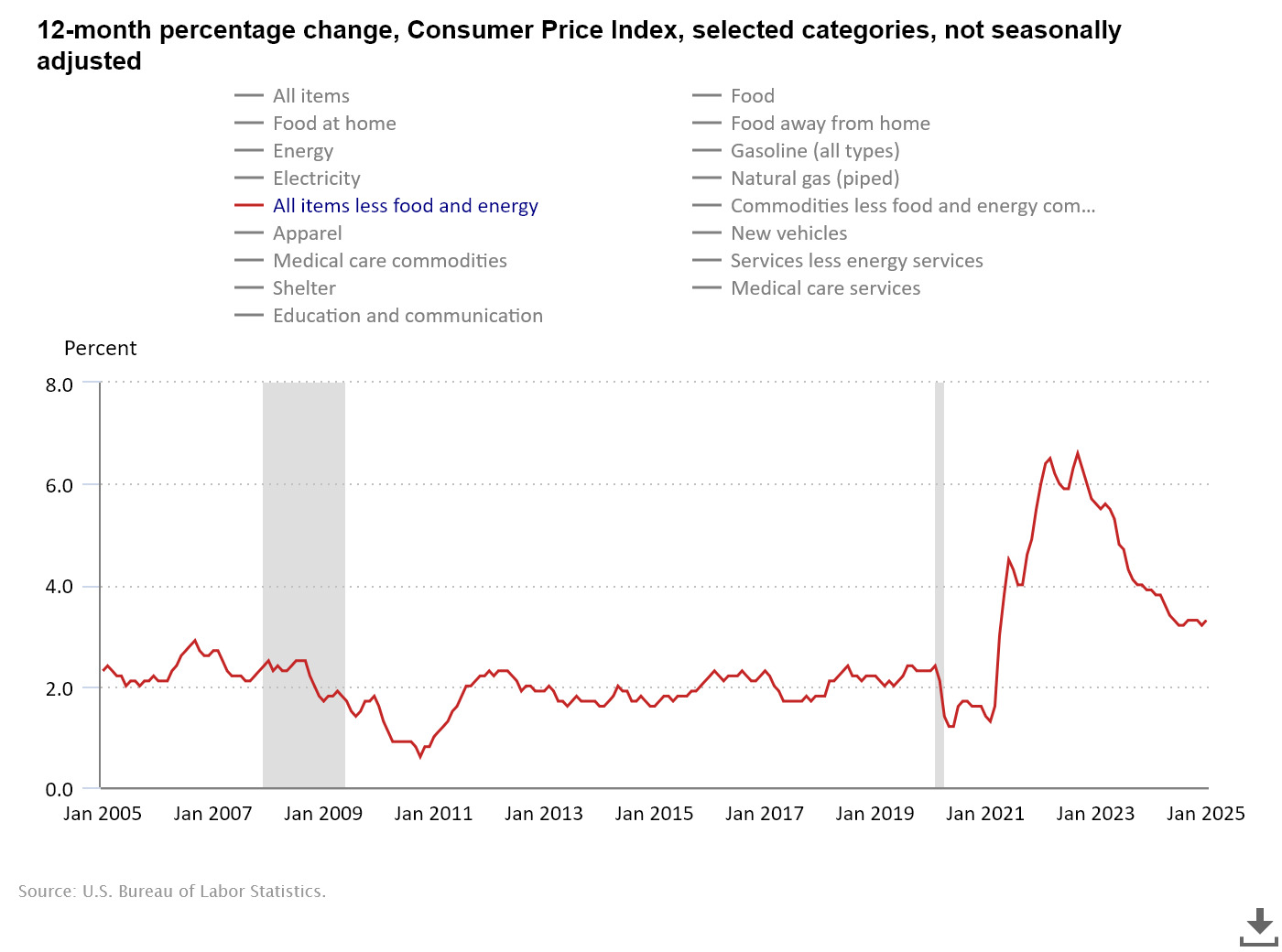

The thought process is tariffs will have an inflationary effect, which I agree they will. When inflation goes up, interest rates go up (or don’t go down further…), and when interest rates go up, the economy is hurt.

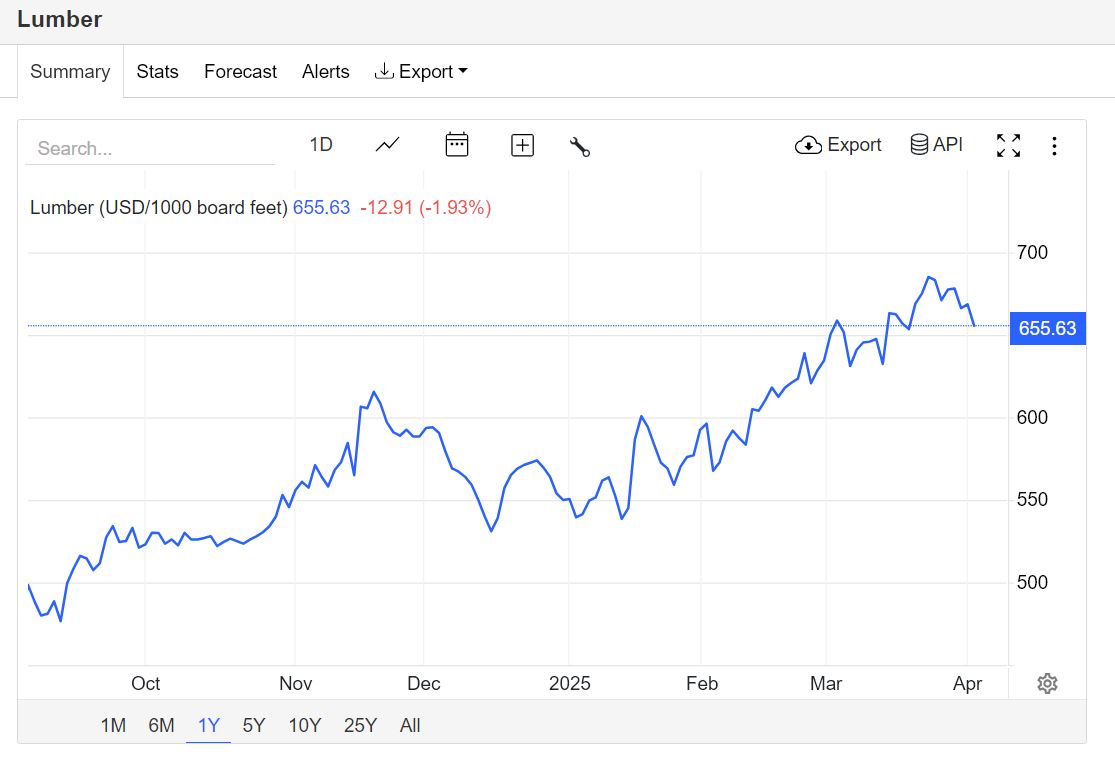

Lets look at the price of lumber, something impacted by tariffs and the cessation of imported lumber from Canada:

As we can see, lumber prices have been climbing steadily, which will have impact on the price of new home construction (which is stagnant anyway), which will trigger other costs that may be captured in CPI and PCE inflation data.

Gold, the classic, “go to” safe haven “currency”, is hitting new highs, reflective of nervousness in stock markets, chart below:

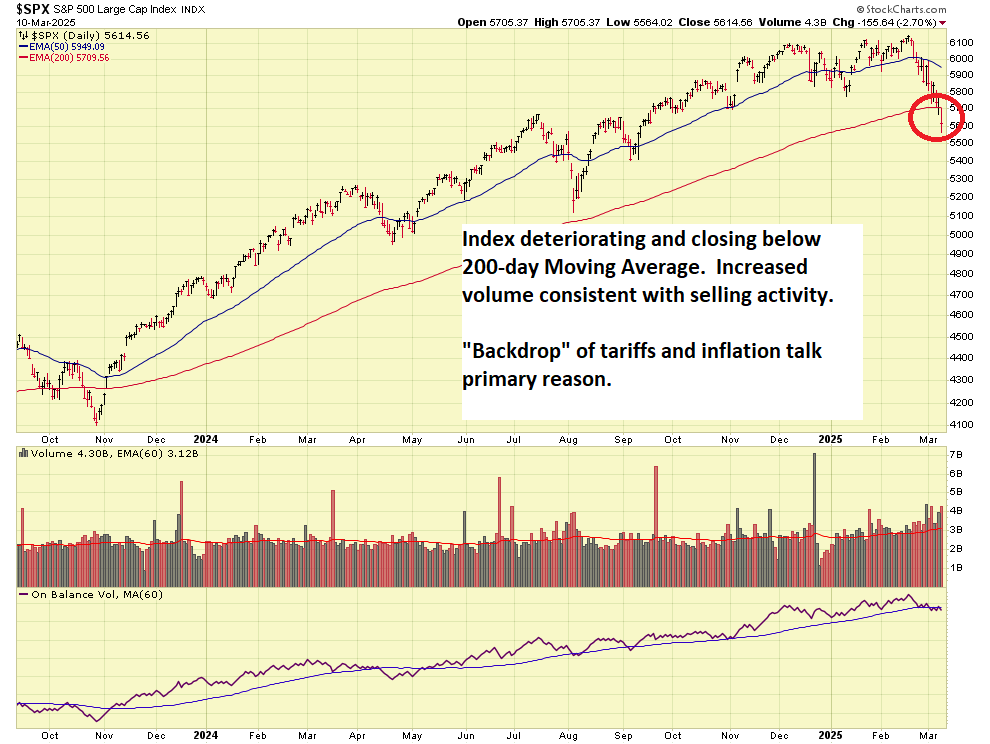

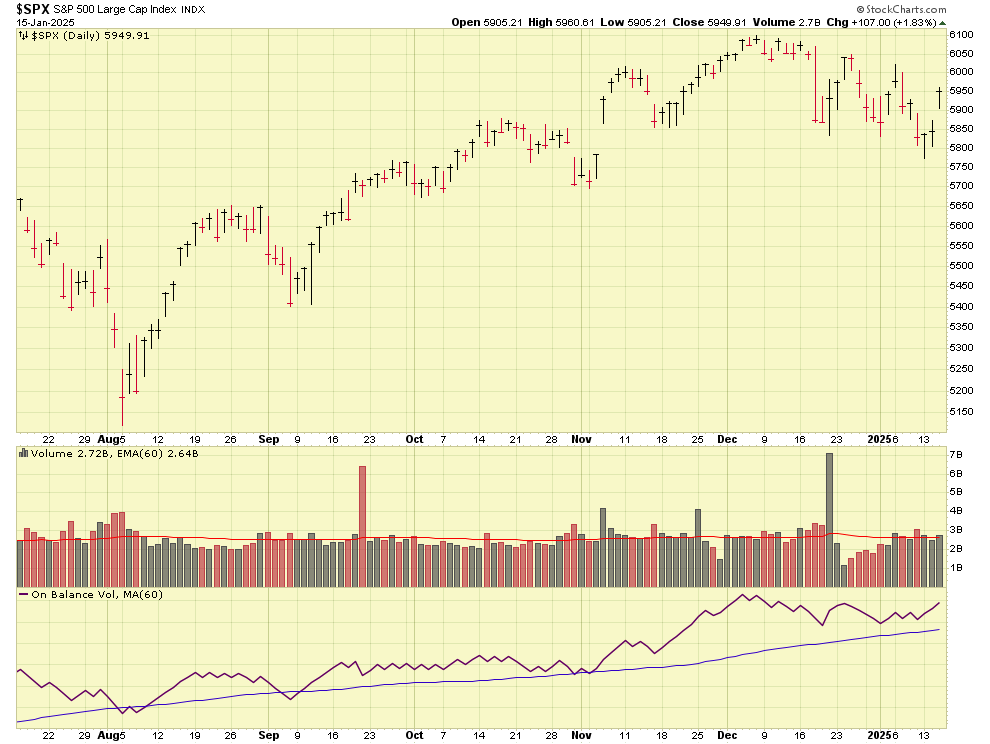

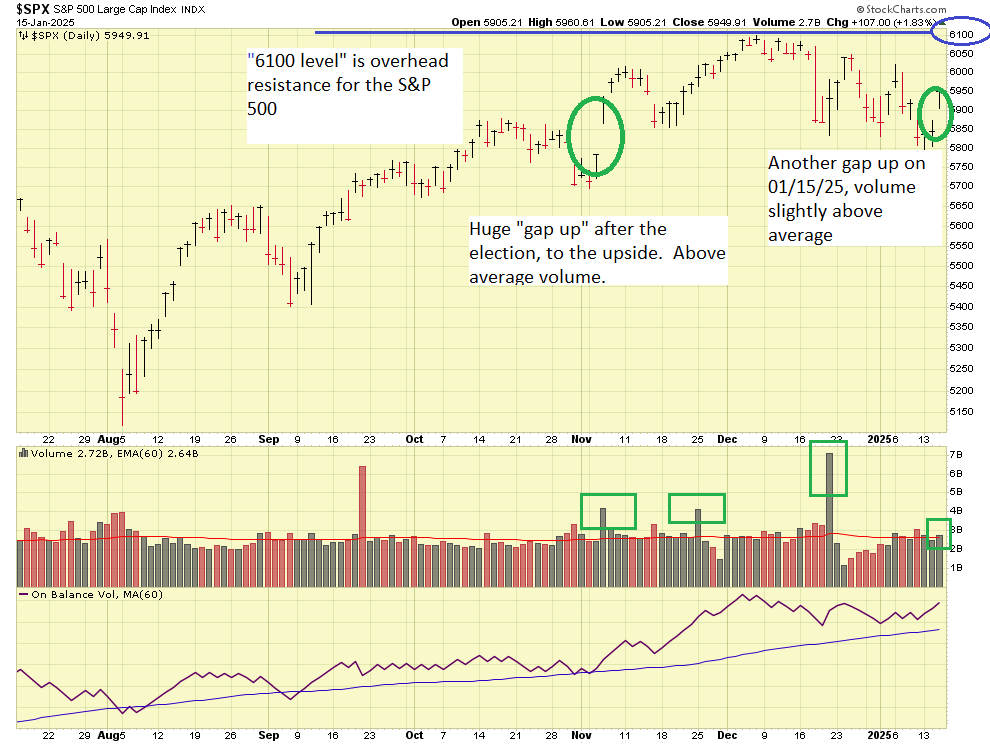

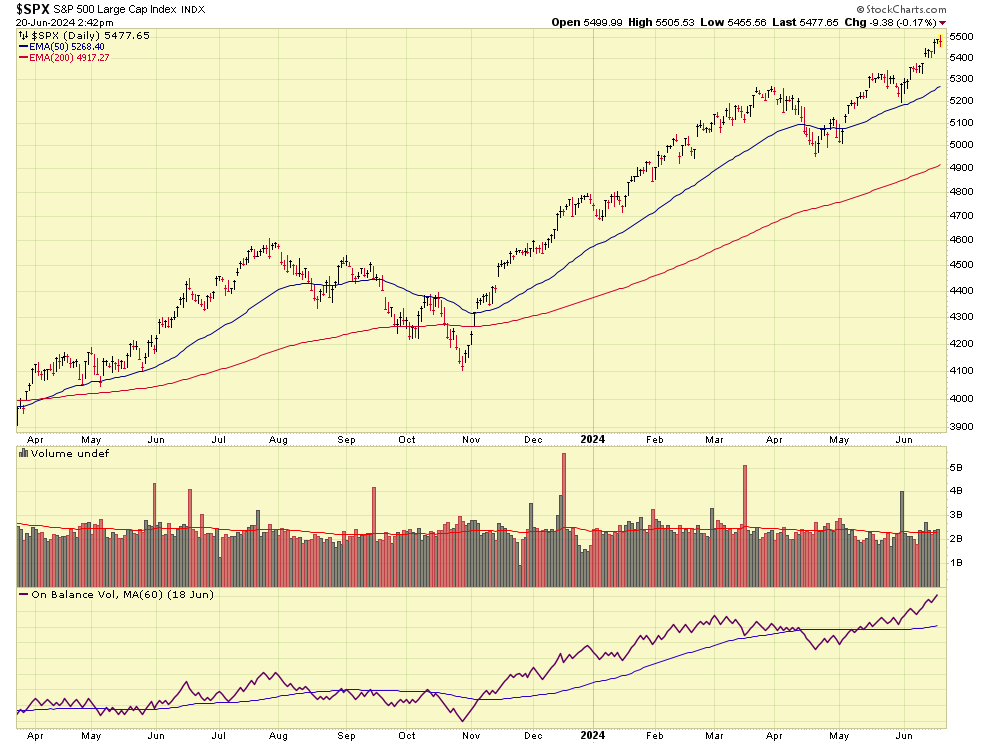

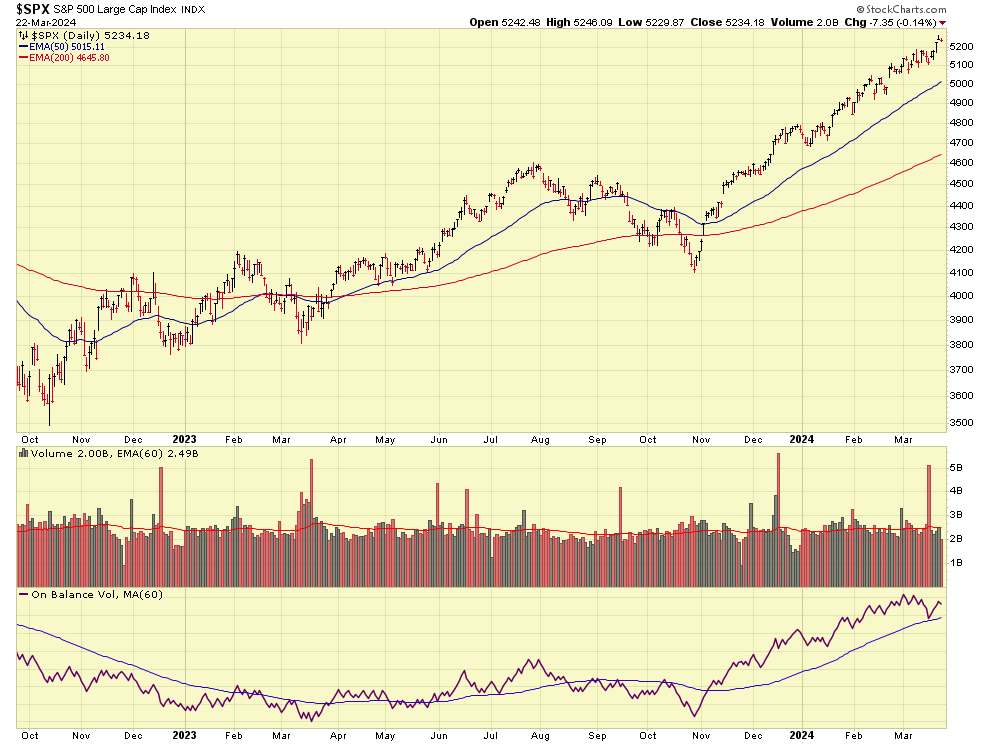

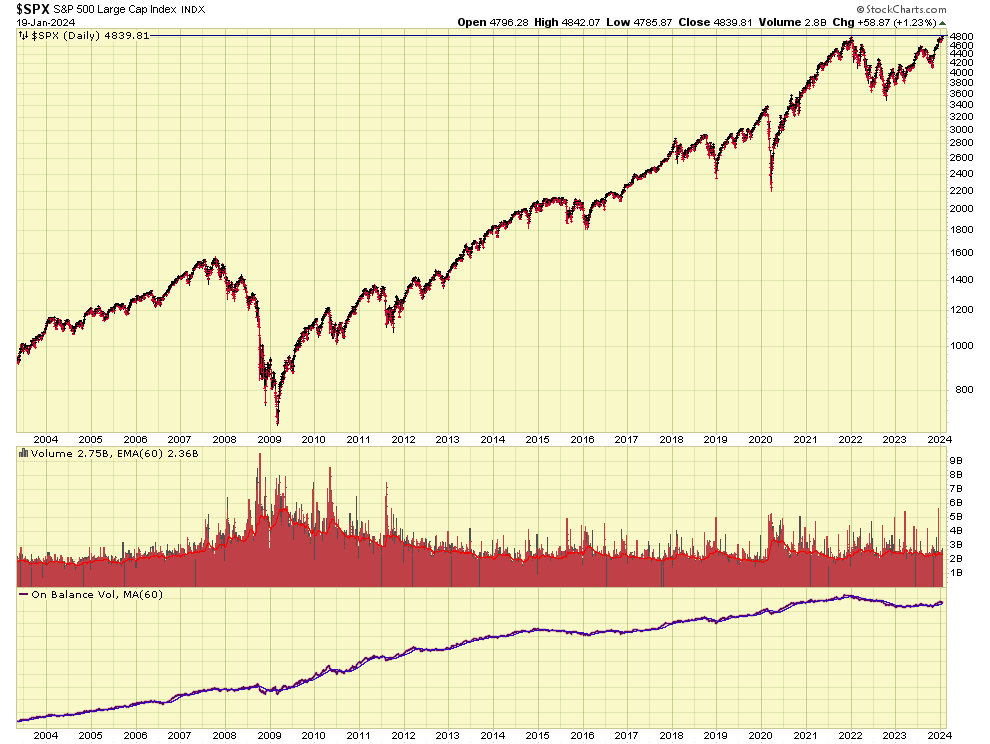

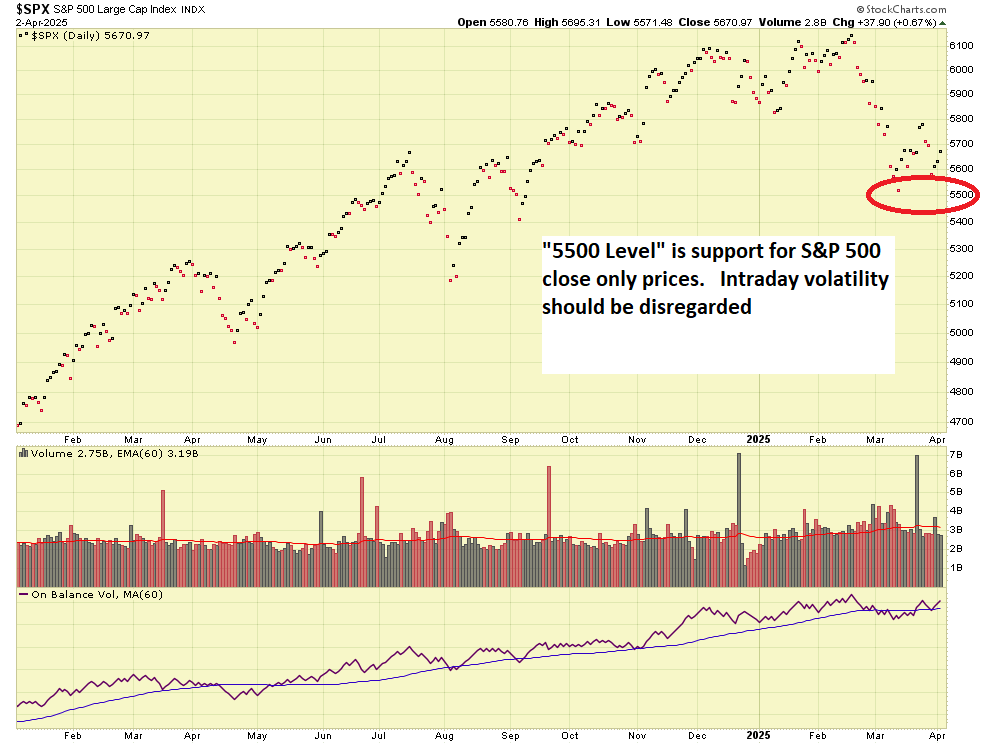

My benchmark index for stocks in the S&P 500: Thousands of mutual funds and retirement plans are invested in it, the biggest companies themselves are part of it (Apple, Wal-Mart, Home Depot,etc), and for a variety of reasons it is my barometer for stock market health. The “support level” to watch is a close below 5500. This is a clear red flag against a healthy market, and continued activity below 5500 is almost a guarantee for a Bear Market to soon exist. See chart:

With that said, what exactly is a Bear Market. I have covered this topic many times over the years, suffice to say it is a 20% decline from a “recent” (within the last 12-24 months) high in a benchmark index. To make it simple, if any of the below indexes hit these levels, that index itself will be considered to be in a “Bear Market”

![]()

In sum, I remain 100% G-Fund, something I moved into back during the first week of March. Here we are, commencing April, and my earlier beliefs remain the same: the market is not in love with the tariffs and technical indicators (chart analysis, etc) are pointing towards a continued downturn. It is what it is.

Thanks for reading, talk to everyone soon

-Bill Pritchard