Good Morning Everyone

I hope this update finds everyone well. I had intended to publish this on Thursday April 20 night, due to my celebratory mood triggered by the Dow Jones closing up 174 points that day. However I said “self, as soon as you publish this, the market will go lower the next day [one of my subscribers, who I personally know, reminds me of this…Hello SJO…]” so I waited until the weekend. The market indeed did go lower, obviously I had nothing to do with it, so maybe loyal follower SJO will be kindler and gentler with me in the future.

With that said, if anything can sum up the market, it is the fact that it is losing confidence in the current administration. Observe that it celebrated things post-election, but the Paul Ryan failed AHCA really kicked it downward. As a recap, on March 23, Paul Ryan’s Health Care reform (basically the repeal of Obamacare) was pulled after Ryan advised President Trump that it would not have the votes for passage. The markets sold off very hard over the next few days, and this laid the ground work for April.

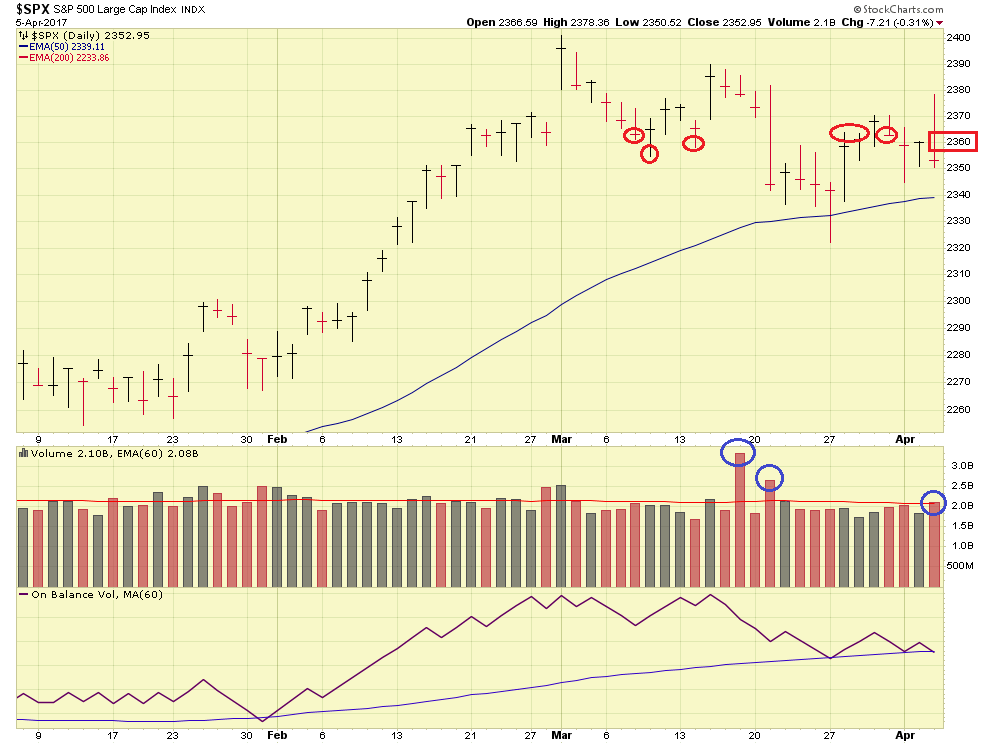

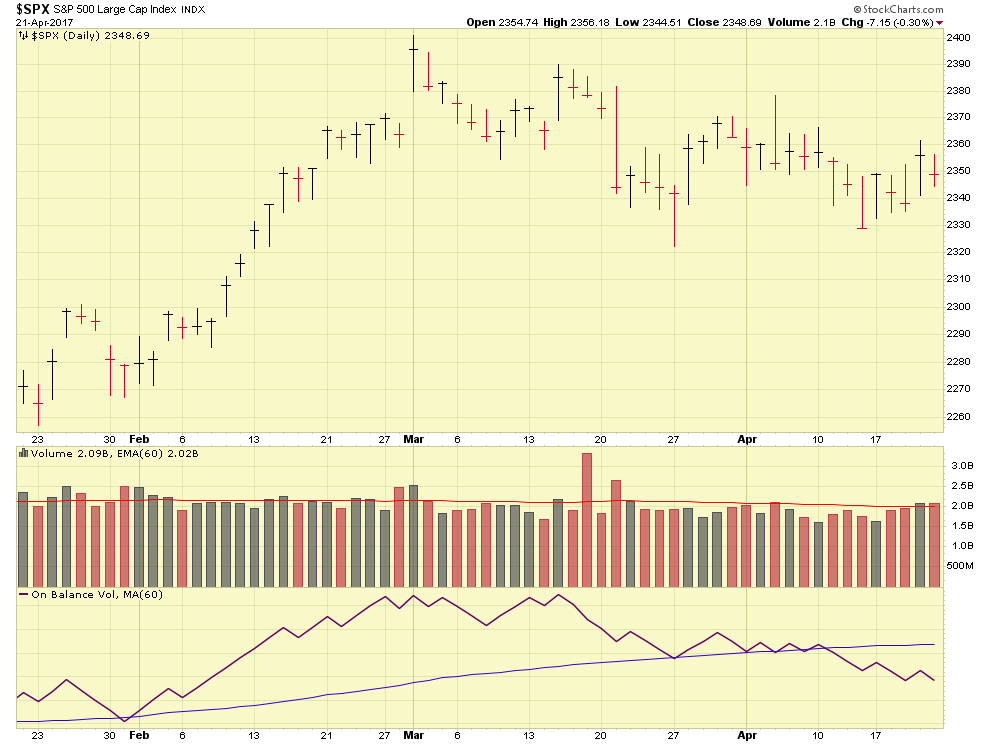

Lets take a look at some charts of the SP 500:

As can be seen, the 2017 peak in the market occurred on March 1, with the SP 500 attaining 2400.98. It then drifted downward, and was pummeled after AHCA failed. I say “failed” because it was never voted on, which is the same as “did not pass” – the markets have since become very skittish and have lost confidence in future administration policies and initiatives oft-mentioned during the elections.

News outlets are reporting that on Wednesday April 26, a “major announcement” on the new tax plan will be released. This week also has a another event, the current Continuing Resolution (CR) expires on April 28.

As I said in numerous posts before, the market is policy driven, and no longer interest rate driven. When was the last time anybody mentioned interest rates ? Exactly my point. Policy, or lack of, is driving events. North Korea, Syria, and other hot-spots do not help matters.

Note that all of April has witnessed low to average volume, indicating that nobody is “getting back into” the market or jumping in with both feet. You have probably three categories of participants right now: the 1) Scared/Non Believers, they are out now, 2) Believers and still in, but getting worried (me), and 3) Those who are out a long time ago or are in only partially, and waiting for the proper time to invest 100%, aka “waiting for the perfect time to enter” (out=not invested, in=yes in stocks and investments- 70% G-Fund and 30% C-Fund would be “partially in.”) The levels to watch are 2335 as a support level on the SP 500, anything below that is a major red flag. The overhead resistance level remains 2360. We cannot begin to celebrate any trend reversal until the index can break upward through that level.

Interestingly, small cap stocks (S-Fund) have responded best on the few days the market has performed well. Overall, my preliminary data reflects that small cap stocks have performed best (or, least-worse) in April. If only we could get a trend change, and we would be good to go.

I remain 100% S-Fund until further advised. Two big events this week, a reported “tax plan announcement” on April 26, and a CR Expiration on April 28. I have no issue jumping to G-Fund but as stormy and cloud as the skies are, I am not quite there yet and remain 100% S-Fund.

I apologize if this post sounds like a political commentary- I did not intend that. However the markets are driven by policy, and its close brother, politics, right now…I felt it was worthy to share my opinion.

Thanks for reading, everybody have a great week.

-Bill Pritchard