Hello Everybody

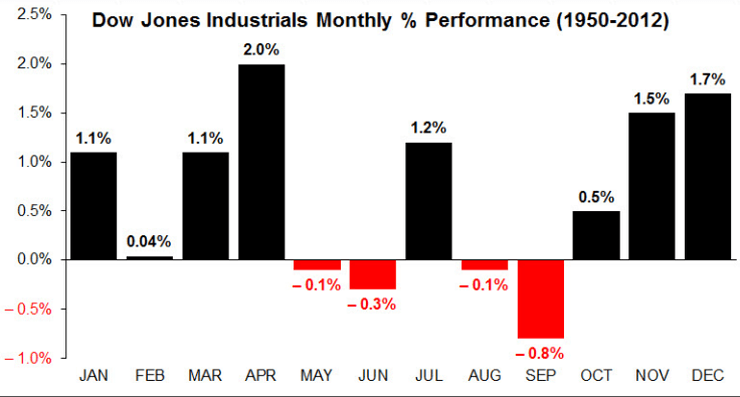

As we enter the month of April, typically the best month of the year for the Dow Jones Index (see image below), we continue to see lethargic performance, mostly believed to be associated with stalled policy making efforts by President Trump. Observe that the month of March, which historically is a positive one, was negative for US stocks and only positive for foreign markets. See image of historical monthly returns:

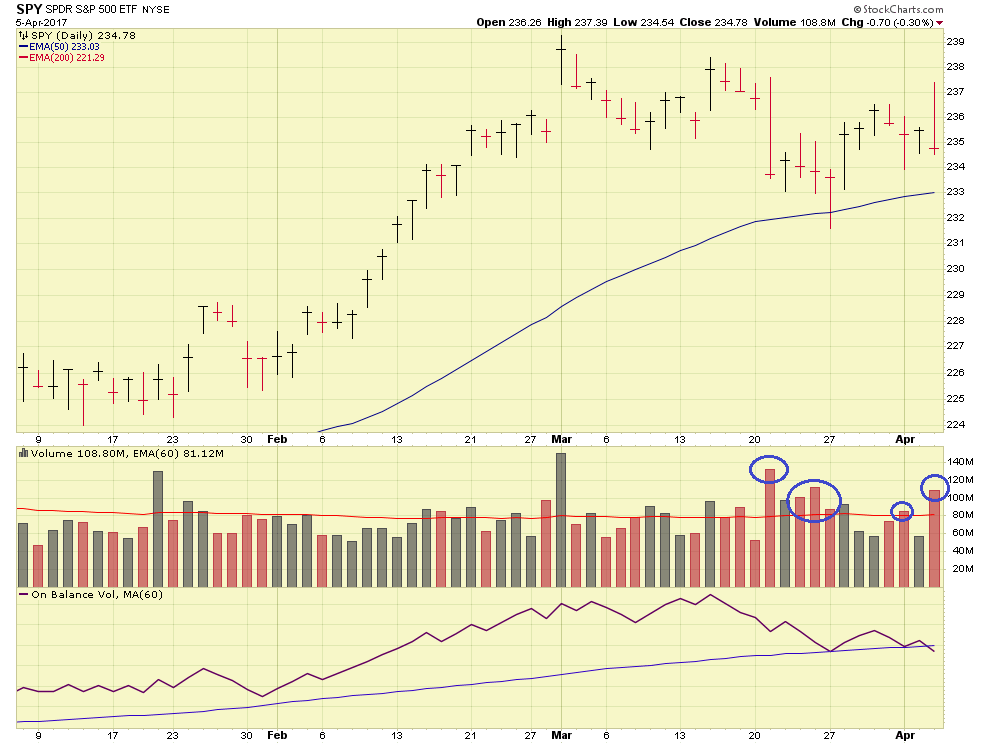

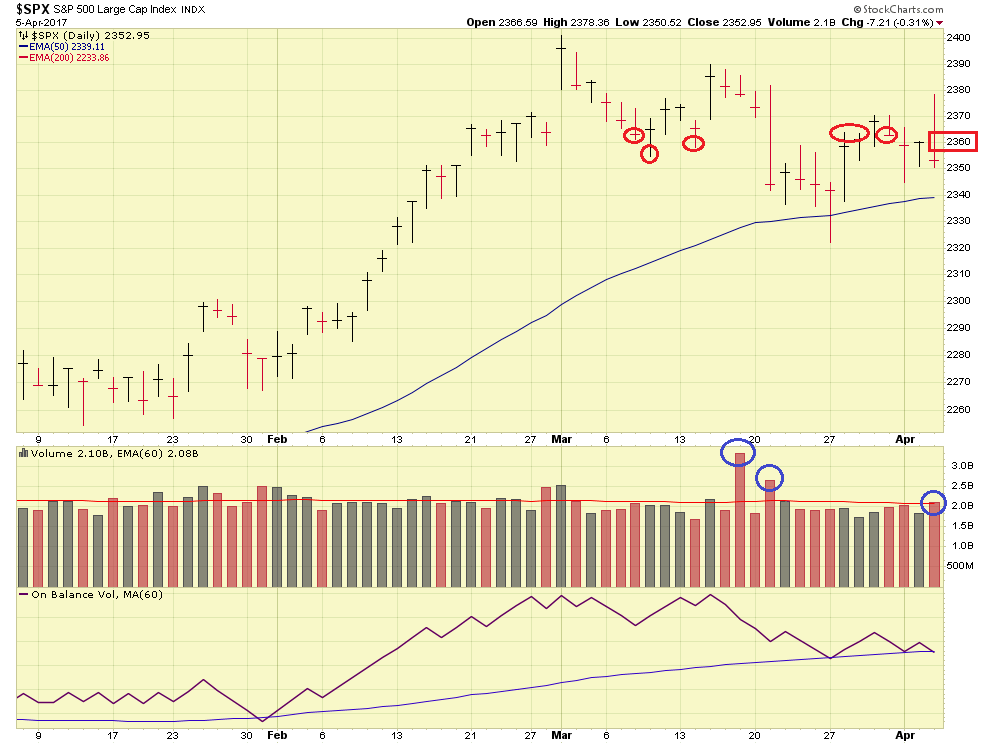

My chosen allocation of 100% S-Fund resulted in a negative March performance. Indeed, the S-Fund, primarily small-cap stocks which are typically listed on the NASDAQ, got beat up pretty good as soon as the believed-to-occur tailwinds for small business suddenly evaporated, soon after Paul Ryan was unable to secure passage of the Affordable Care Act. Let’s take a look at some charts, which unfortunately display above average volume with price movement to the downside, which means “selling” or “distribution” on the indexes. The SP-500 chart and the SPY ETF is displayed, as volume activity is often more apparent via the SPY ETF.

Apparent in the charts is that we have had at least six distribution days since March 20. Note that a high distribution day count has the potential to turn an uptrend into a downtrend, and a subsequent bear market condition. We are not there yet but clearly I am not over joyed about the current situation.

The key level on the SP-500 remains 2360, this was mentioned in prior posts however it remains an important area to watch. In recent days the index has penetrated this level, only to fall back down through it. Market action on 04-05-17 was positive in the morning, upon the release of a strong Jobs Report, with 263,000 jobs added, much higher than the original believed amount of 170-185,000. Unfortunately, the market now remains susceptible and largely news-driven, a motorless boat in the ocean, quick to react to any light blinking from the shore: Federal Open Market Committee (FOMC) Minutes released during the afternoon, indicating potential interest rate hikes in 2017, quickly sent the market back downward.

I stated the following in my 02-05-17 post:

“….the markets are no longer interest-rate driven, they are now policy-driven, policies and positions being advocated by Mr. Trump and Congress….”

I strongly feel this remains the case, however I want to insert that “lack of policy” is sure to drive the markets south. If we continue to have lack of policy passage, and lack of agreement in Washington, the markets could continue lower.

Until then, I remain 100% S-Fund: accepting the fact that March was negative, once we get unstuck and things in Washington (hopefully) get resolved, the small caps will take off higher, in my opinion. Again, I remain 100% S-Fund.

Thank you for reading and please continue to share this site with your friends and colleagues.

-Bill Pritchard