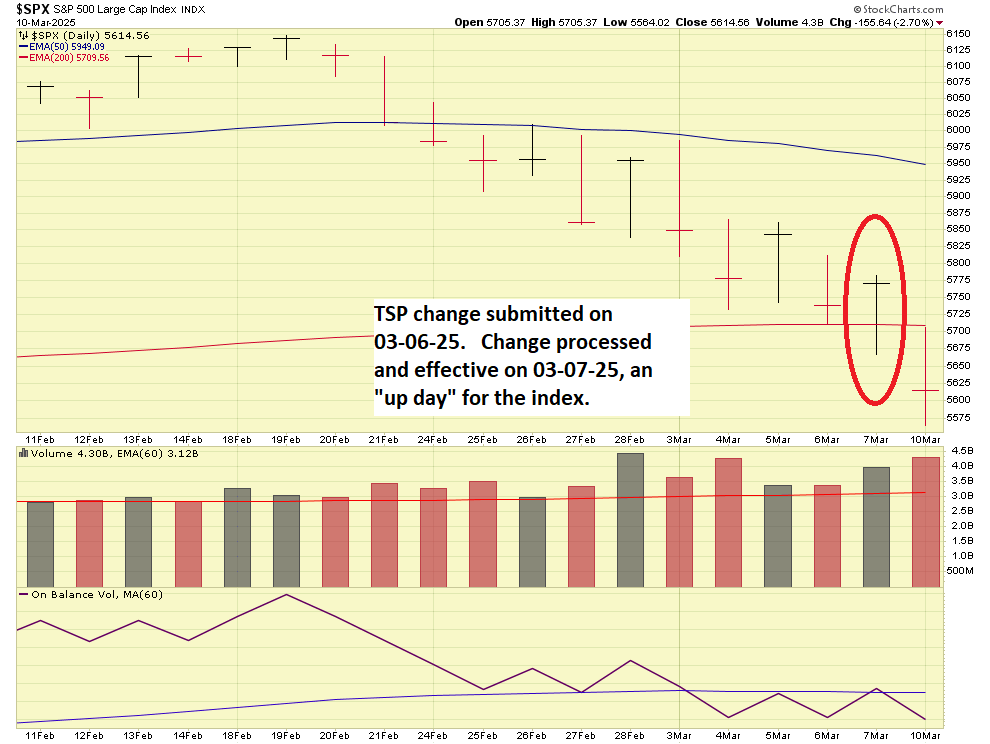

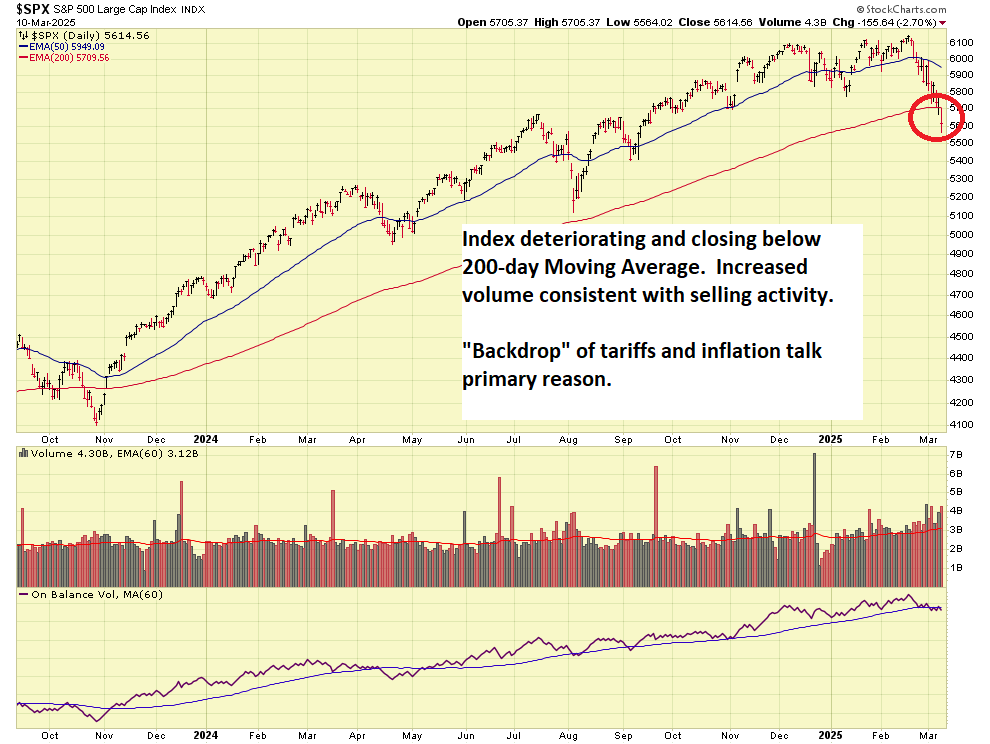

As most know, the last few days have been rather brutal in the markets. On March 6, I submitted my change request to move to 100% G-Fund, which (shockingly) took effect on March 7. Today, March 10, the Dow Jones index closed 890 points to the downside (losing up to 1,100 points intraday). The S&P 500 index and NASDAQ also all closed lower:

Clearly, the reasons behind this remain “Tariff Talk” and inflation concerns. As we know, tariffs could potentially cause inflation to tick higher. They also could potentially have a COVID-like effect (remember grocery store shelves devoid of toilet paper) on products. If Canadian lumber is shut off, American lumber producers cannot turn on the spigot full bore overnight…this will result in a supply shortage as production (supply) may not be able to keep up with demand. High priced housing and new home construction (lack of…) may fix this problem in this particular example (because the lumber demand is softened) but you get the point. So does Wall Street. And they are “speaking” with their trading activity.

On Wednesday March 12, at 8:30 PM Eastern, the “CPI” will be released. Often discussed here, inflation (a great post from 2018 is here) is also tied to interest rates. If inflation is rising, the Federal Reserve may be inclined to PAUSE further rate cuts at the minimum, and at the worse, RAISE interest rates. In sum, rising inflation is not embraced by the markets. A quick search of business news reflects that 2.9% is the expected “Headline CPI” or “CPI” reading. This is not “Core CPI” which is CPI without fuel and food.

Should we see CPI come in at 3.0%, the market will likely go down. It WILL go down if CPI is 3.1, 3.2% or more. Pray that does not happen. CPI release can be found here

With that said, I conclude this post. Tariff and inflation concerns rule the markets, and major fund managers are not “waiting to find out” and are exiting positions.

Have a great week and thanks for reading

-Bill Pritchard